All Categories

Featured

Table of Contents

These functions can differ from company-to-company, so be certain to explore your annuity's fatality benefit attributes. A MYGA can mean lower tax obligations than a CD.

At the very the very least, you pay taxes later on, rather than sooner. Not only that, but the compounding interest will be based upon an amount that has not currently been strained. 2. Your recipients will certainly get the complete account worth as of the day you dieand no abandonment charges will certainly be subtracted.

Your beneficiaries can choose either to get the payment in a swelling amount, or in a series of income settlements. 3. Often, when a person passes away, also if he left a will, a judge decides who obtains what from the estate as in some cases loved ones will certainly say regarding what the will ways.

With a multi-year set annuity, the proprietor has actually plainly marked a recipient, so no probate is needed. If you add to an IRA or a 401(k) strategy, you receive tax deferment on the incomes, simply like a MYGA.

Is An Annuity Considered Life Insurance

So if you are younger, spend just the funds you will not need up until after age 59 1/2. These can be 401(k) rollovers or money you keep in individual retirement account accounts. Those items currently use tax deferment. MYGAs are wonderful for people that wish to stay clear of the risks of market fluctuations, and want a taken care of return and tax deferral.

When you select one, the passion rate will certainly be taken care of and guaranteed for the term you select. The insurance company invests it, typically in top quality long-term bonds, to money your future settlements under the annuity. That's since bonds are quite risk-free. However they can likewise buy stocks. Bear in mind, the insurer is counting not simply on your private payment to money your annuity.

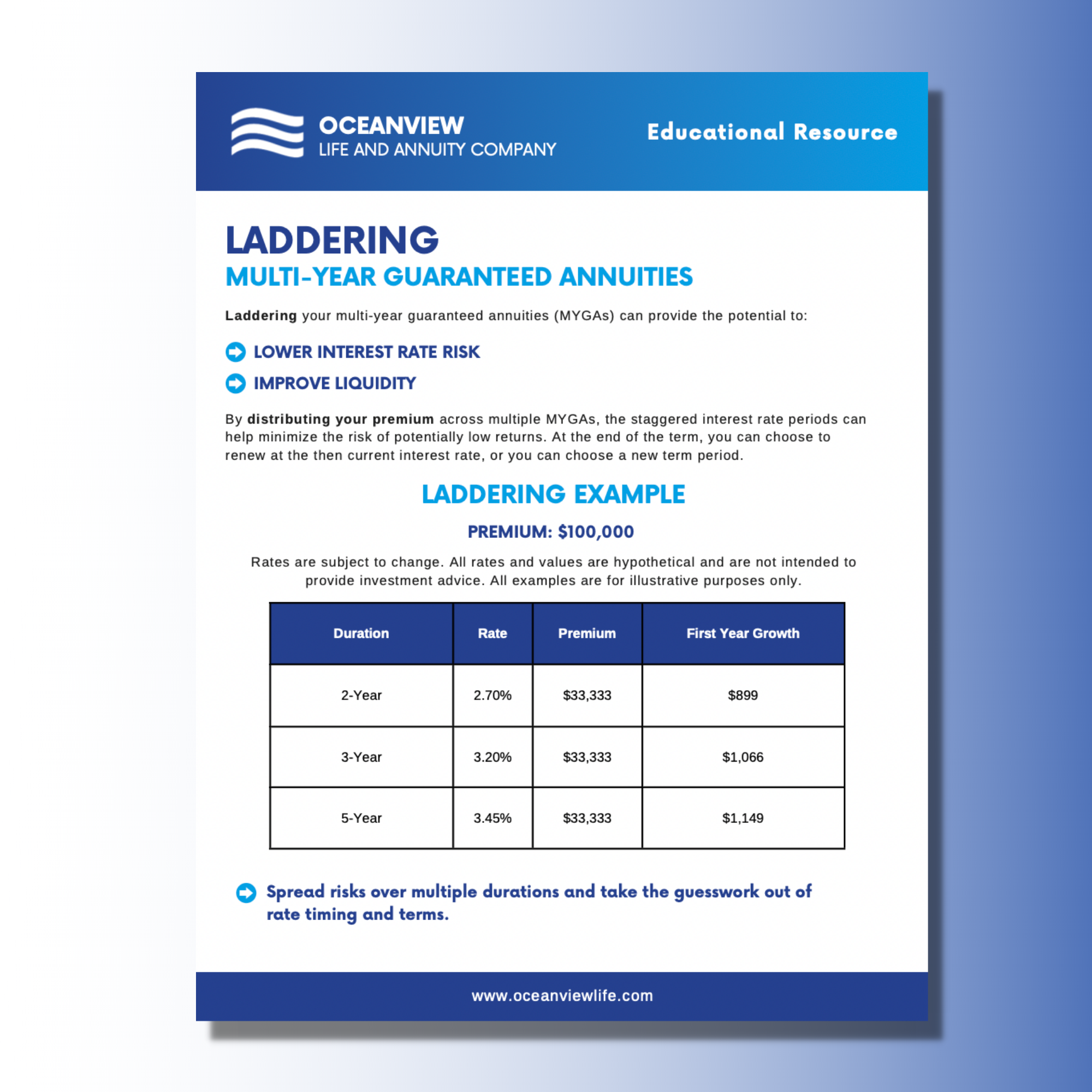

These payments are developed into the purchase rate, so there are no covert fees in the MYGA contract. In reality, postponed annuities do not bill fees of any type of kind, or sales fees either. Sure. In the recent setting of reduced passion rates, some MYGA financiers construct "ladders." That indicates buying numerous annuities with staggered terms.

Retirement Annuity Payout

If you opened up MYGAs of 3-, 4-, 5- and 6-year terms, you would have an account growing each year after 3 years (guaranteed future income annuity). At the end of the term, your cash might be taken out or placed right into a brand-new annuity-- with luck, at a greater price. You can additionally make use of MYGAs in ladders with fixed-indexed annuities, an approach that looks for to maximize return while additionally protecting principal

As you compare and contrast images provided by numerous insurer, take into consideration each of the areas listed over when making your decision. Recognizing agreement terms as well as each annuity's benefits and downsides will allow you to make the finest choice for your financial circumstance. Believe carefully concerning the term.

Fixed Annuities Safe

If interest prices have actually climbed, you might wish to lock them in for a longer term. Most state laws permit you at the very least 10 days to change your mind. This is called a "complimentary look" duration. During this time around, you can get every one of your refund. This must be prominently stated in your agreement.

The business you buy your multi-year assured annuity with accepts pay you a set rate of interest on your costs amount for your selected period. You'll get interest credited often, and at the end of the term, you either can restore your annuity at an updated rate, leave the cash at a taken care of account rate, elect a negotiation option, or withdraw your funds.

What Is A Deferred Lifetime Annuity

Given that a MYGA provides a set rates of interest that's guaranteed for the agreement's term, it can provide you with a foreseeable return. Security from market volatility. With prices that are established by agreement for a details number of years, MYGAs aren't subject to market variations like various other financial investments. Tax-deferred development.

Restricted liquidity. Annuities normally have charges for early withdrawal or surrender, which can restrict your capability to access your money without fees. Lower returns than various other financial investments. MYGAs may have lower returns than supplies or common funds, which could have greater returns over the lengthy term. Fees and expenditures. Annuities generally have surrender costs and management prices.

MVA is an adjustmenteither favorable or negativeto the accumulated value if you make a partial surrender above the free quantity or totally surrender your contract throughout the surrender cost period. Since MYGAs offer a set rate of return, they may not keep rate with inflation over time.

Annuity Commissions Rates

:max_bytes(150000):strip_icc()/Term-a-annuity-d4d5906faea940828244ef128f416cc5.jpg)

It is very important to vet the toughness and security of the firm you choose. Consider reports from A.M. Best, Fitch, Moody's or Standard & Poor's. MYGA prices can change frequently based upon the economy, but they're normally greater than what you would gain on an interest-bearing account. The 4 sorts of annuities: Which is right for you? Need a refresher on the four basic sorts of annuities? Find out a lot more exactly how annuities can assure a revenue in retirement that you can't outlive.

If your MYGA has market value change arrangement and you make a withdrawal prior to the term is over, the business can adjust the MYGA's abandonment value based on adjustments in rates of interest - cashing in annuities. If rates have actually raised since you purchased the annuity, your surrender worth may reduce to make up the higher rate of interest setting

Not all MYGAs have an MVA or an ROP. At the end of the MYGA period you have actually chosen, you have 3 alternatives: If having an assured passion price for a set number of years still straightens with your financial technique, you just can restore for another MYGA term, either the same or a different one (if offered).

With some MYGAs, if you're unsure what to do with the cash at the term's end, you don't have to do anything. The collected worth of your MYGA will relocate right into a taken care of account with an eco-friendly one-year rate of interest determined by the firm - sell annuity calculator. You can leave it there up until you select your following action

While both deal guaranteed rates of return, MYGAs typically use a greater interest price than CDs. MYGAs expand tax obligation deferred while CDs are taxed as income every year.

With MYGAs, surrender fees may use, depending on the kind of MYGA you choose. You might not just shed passion, however additionally principalthe money you originally contributed to the MYGA.

Life Insurance Annuities Explained

This indicates you might weary yet not the primary quantity added to the CD.Their conservative nature usually allures extra to individuals that are coming close to or currently in retirement. But they might not be best for everybody. A may be ideal for you if you want to: Make the most of an ensured rate and lock it in for a period of time.

Benefit from tax-deferred profits development. Have the option to choose a settlement choice for a guaranteed stream of earnings that can last as long as you live. As with any type of financial savings vehicle, it is necessary to very carefully assess the conditions of the item and consult with to establish if it's a smart option for accomplishing your private needs and objectives.

1All guarantees including the survivor benefit repayments depend on the claims paying capability of the issuing business and do not use to the investment performance of the hidden funds in the variable annuity. Properties in the underlying funds are subject to market risks and may vary in worth. Variable annuities and their underlying variable financial investment choices are sold by program only.

How To Get Out Of An Annuity Fund

Please review it prior to you spend or send out money. 3 Present tax obligation legislation is subject to interpretation and legal modification.

Entities or persons dispersing this details are not accredited to provide tax or legal recommendations. People are urged to look for specific suggestions from their individual tax obligation or legal advise. 4 , Exactly How Much Do Annuities Pay? 2023This material is intended for general public use. By giving this content, The Guardian Life Insurance Policy Firm of America, The Guardian Insurance Policy & Annuity Company, Inc .

{kind=link}

Table of Contents

Latest Posts

Breaking Down Your Investment Choices Everything You Need to Know About Variable Vs Fixed Annuity Breaking Down the Basics of Investment Plans Benefits of Tax Benefits Of Fixed Vs Variable Annuities W

Exploring the Basics of Retirement Options A Comprehensive Guide to Deferred Annuity Vs Variable Annuity Breaking Down the Basics of Fixed Index Annuity Vs Variable Annuity Advantages and Disadvantage

Breaking Down Variable Vs Fixed Annuity A Comprehensive Guide to Investment Choices What Is Deferred Annuity Vs Variable Annuity? Pros and Cons of Various Financial Options Why Choosing the Right Fina

More

Latest Posts